SaaS Capital 2021 Recap and Look Ahead

[ad_1]

No one knew what to expect going into 2021. Sure enough, the year delivered an unpredictable potpourri of economic extremes and indicators. But overall, 2021 was generally a great year to be running a SaaS company. Myriad factors pulled and pushed the broad economy, and individual industries specifically, in different ways – sometimes from one historic extreme to another! It’s worth zooming (way) out here, because these last two years really are unprecedented.

Stimulus

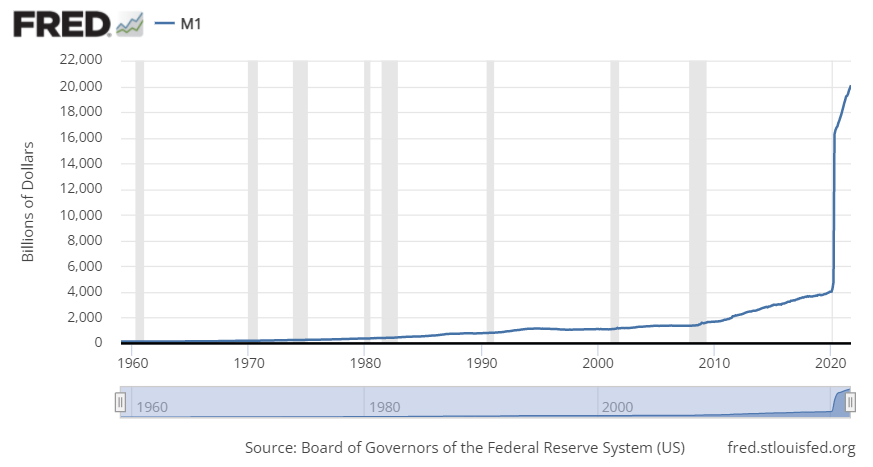

The biggest influence on markets, and indeed on the world economy, has been the US government’s monetary and fiscal response to the pandemic. Through the largest single relief package in history (at $2.3 trillion), the US money supply jumped 4.5x in 6 weeks from March to May 2020. Subsequent programs like the American Rescue Plan have continued to push the money supply to 5x its pre-pandemic level.

- The chart below shows the US money supply from 1960 to today. This absolutely gargantuan COVID stimulus is clearly visible as a “wall of cash.”

- All but two SaaS Capital portfolio companies (and many other SaaS companies we have spoken with) took PPP or EIDL loans, and all of those were forgiven in their entirety. Anecdotally, those programs, while not perfect, were highly effective at the goal of reducing or delaying employee layoffs.

Inflation

The flip side of the stimulus coin is inflation, perhaps the most controversial macroeconomic topic of 2021 – largely because annual measures are eye-popping when based on the largely deflationary environment during 2020.

- Consumer prices are up 7% from a year ago, which would be the highest inflation rate since the early 1980s – except prices are only up 8% from two years ago, making the average a less impressive, though still elevated, 3.9% per year.

- An ideological battle rages among economy-watchers about how real and permanent this inflation is, with the word “transitory” becoming 2021’s impolitic word to broach among dinner guests. Without picking sides, we can observe that if inflation doesn’t subside “on its own,” continued high inflation would ultimately prompt the Fed to raise rates, in turn slowing investment and growth.

Growth

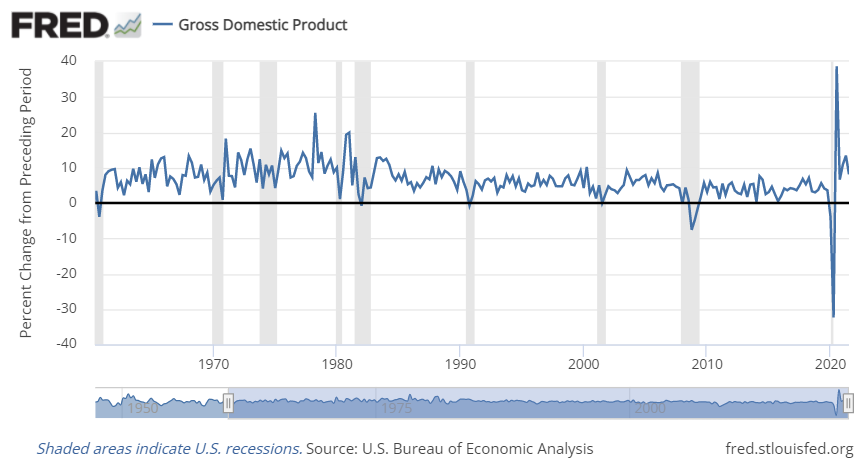

Speaking of growth, following the sharp drop off in Gross Domestic Product in March and April 2020, GDP has surged – at its highest rate of growth since World War II. The economy in 2021 remained red hot and it was a good year to be in business.

Supply Chain

Through 2020 and 2021 supply chains were whipsawed. Global lock-downs forced production and shipping to cease, followed abruptly by the biggest demand surge in 50 years.

- SaaS companies that sell hardware along with their software are seeing delays and cost increases, and many SaaS companies were indirectly impacted by the supply chain issues through their customers. But most have avoided any direct issues.

Workforce

One macro-economic area that has impacted SaaS companies, and likely will continue to be a challenge well into 2022, is the labor market.

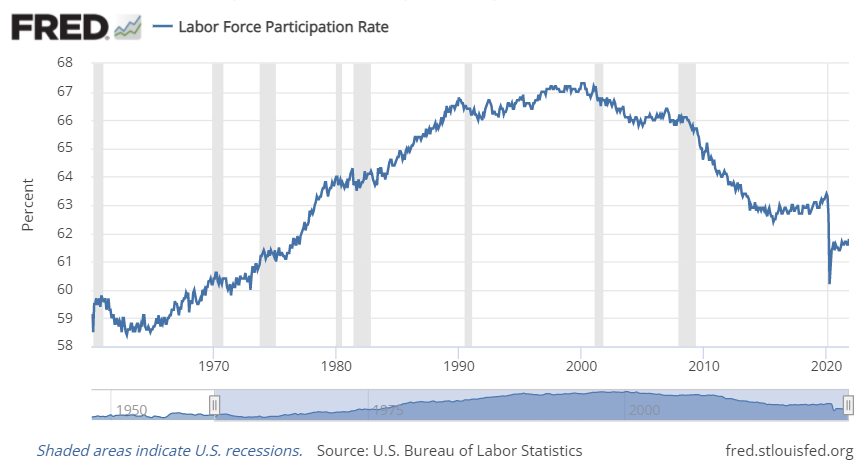

- Below is a chart of labor force participation, where you can clearly see we remain well-below pre-pandemic levels (the broader downward trend over the last 20 years is a result of Baby Boomer retirements).

- Numerous portfolio companies are experiencing the “Great Resignation” first hand and having trouble (re)filling roles. We’ve heard employees leaving for new jobs paying 30-40% more.

- Companies are doing whatever they can to retain employees, and the most recent (December 9, 2021) unemployment report showed new jobless claims at the lowest level since 1969 – no one is daring to lay anyone off in this market.

- Able employees, particularly tech workers, have the upper hand and are demanding – and getting – salary and work-life concessions. Now more than ever, keep and compensate your good employees, or you may not see them tomorrow.

So Where Did All of These Factors Take the SaaS Industry in 2021?

Industry – Macro

Through 2020 and 2021, Software-as-a-Service proved to be a very pandemic-resilient business model.

- Logistically

- Cloud software is tailor-made for remote work, and since many companies already were at least partially remote, they could move to fully remote in days, if not hours. Furthermore, SaaS systems-of-record and workflows have become even more important during this workforce reshuffling. It’s now harder (and more inadvisable) than ever to rely on an old Windows program or Excel macro on Bob’s desktop two cubicles down – since nobody’s in their cubicle anymore, and Bob has changed jobs for a 40% raise anyway.

- Financially

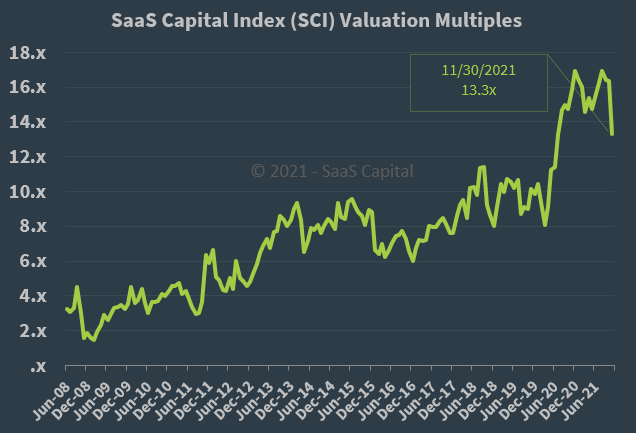

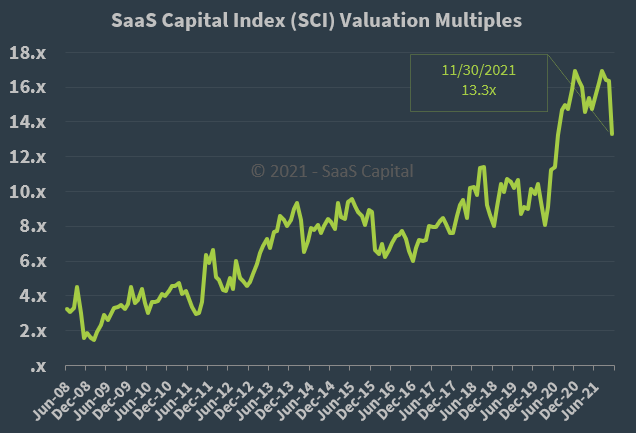

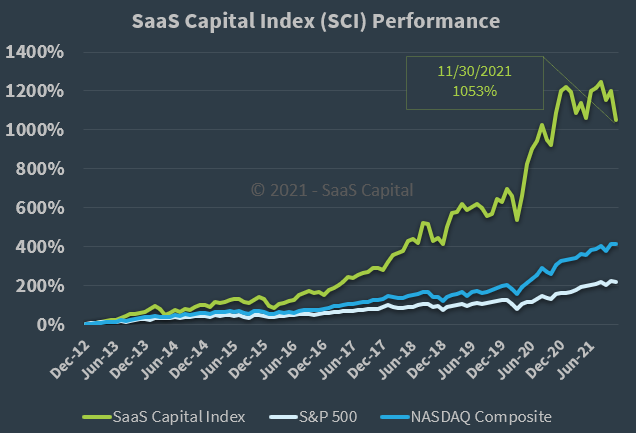

- While the broad stock market has boomed since Q2 2020, investors continued to see superior value and safety in B2B SaaS companies. Our SaaS Capital Index, which tracks approximately 65 public B2B SaaS companies, rose even faster than the broader indices through 2020, but has held fairly flat through most of 2021. The median valuation multiple of the 65 public B2B SaaS companies in the SaaS Capital Index was about 16 times run-rate ARR for the previous 12 months until a November 2021 pull-back, when it dropped to 13.3x ARR.

- Public and private capital markets were extremely active in 2021. It is on pace to be a record year for M&A activity with over 1,300 SaaS transactions, including the very large PE buyouts of Proofpoint, QAD, Boomi, and FireEye.

- Our experience mirrored the broader industry: eleven portfolio companies raised capital or sold their business outright in 2021.

- Private SaaS valuation multiples were higher than historic trends, as they were pulled up by the public comparables, though private multiples trailed the public multiples’ increase. We saw the typical discount from the public median valuation to the valuation in these transactions widen from approximately 28% to approximately 50%.

- While the broad stock market has boomed since Q2 2020, investors continued to see superior value and safety in B2B SaaS companies. Our SaaS Capital Index, which tracks approximately 65 public B2B SaaS companies, rose even faster than the broader indices through 2020, but has held fairly flat through most of 2021. The median valuation multiple of the 65 public B2B SaaS companies in the SaaS Capital Index was about 16 times run-rate ARR for the previous 12 months until a November 2021 pull-back, when it dropped to 13.3x ARR.

Companies – Micro

SaaS Capital’s annual peer survey and our close contact with our portfolio gives us a unique, detailed perspective on how SaaS companies themselves experienced the pandemic in 2020 and 2021. We found a negative impact on SaaS companies, but a far milder effect than the larger economy experienced.

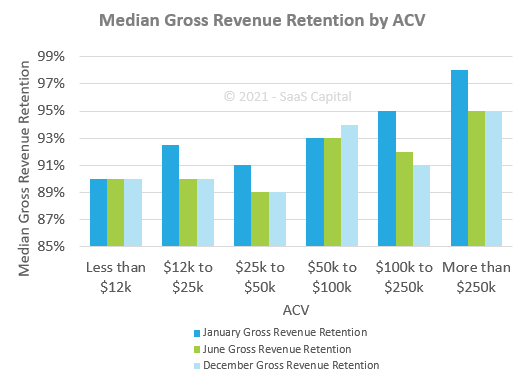

![Median Gross Revenue Retention by ACV 2021 SaaS Capital]() Retention

Retention

- Retention rates for private, B2B growth-stage SaaS companies dipped slightly in Q2, but only very slightly. We’ve mentioned above some reasons why SaaS logically should be “sticky” despite the COVID downturn, and this data seems to bear it out well. Read more on 2020 retention here.

- Growth

- Growth rates in 2020 were lower by about 10 percentage points than they were in 2019 (30% annual growth versus 40% in 2019, for growth-stage SaaS companies). Thirteen percent of surveyed companies saw flat or shrinking revenue in 2020, versus just 2% in 2019. Read more on growth rates here.

- Throughout 2021 we saw growth improving from 2020, but sales cycles were longer than pre-pandemic, and companies that relied on trade shows and other in-person lead generation struggled to fill the top of the funnel.

- Retention and Recruiting

- Anecdotally, as mentioned above, employee retention and recruiting is the biggest challenge most SaaS companies faced in the second half of 2021.

Retention

Retention

SaaS Capital

Despite elevated valuations and a glut of equity investor dry powder, SaaS Capital’s MRR-based credit facility continued to resonate with SaaS founders and operators. More SaaS companies than ever approached us in 2021 looking for a tool to boost growth to an equity fundraising or outright exit.

- We added 10 new portfolio companies so far in 2021 and have signed term sheets with 4 other companies that are in the final stages of closing.

Outlook

Looking ahead, what do we predict for the SaaS market in 2022?

- Inflation, and the Fed’s reaction to it, if any, is the biggest question mark for 2022. If demand softens and/or supply chains recover, inflation may abate on its own and 2022 could be a great year. If not, and inflation worsens, and the Fed is forced to raise interest rates, it could be a choppy macro-economic environment.

- Wages will likely stay elevated through 2022. There is nothing that points to a significant softening in the labor market, particularly not for SaaS-experienced engineering, sales, marketing or support people.

- The way information work gets done has undergone a sea change. Remote or hybrid work is likely here to stay. Google and Amazon continue to postpone their Return To Office date, recently revised to late Q1 2022. They will likely eventually require some in-person office work, but the last two years have proven that employees can be just as productive at home and the quality of life can be vastly improved (those with small children notwithstanding).

- The broader market will continue to re-open and loosen – supply chains should normalize by summer 2022, barring any additional global supply or demand shocks. [“barring” is doing a lot of work here!!]

- The broader stock market may soften slightly after a very heated 18 months, and we would not be surprised to see valuations slide further, but as this entire post has tried to highlight, the economy and capital markets are a) not the same thing! And b) in unprecedented times. It’s difficult to predict how the next year will unfold. But that is a takeaway in itself: be prepared for anything and be ready to shift if the market softens or accelerates.

- 2022 will again be a great year for building a SaaS company, as our economy continues its secular shift toward on-demand software as the “operating system” of our complex modern life.

![]()

[ad_2]

Source link